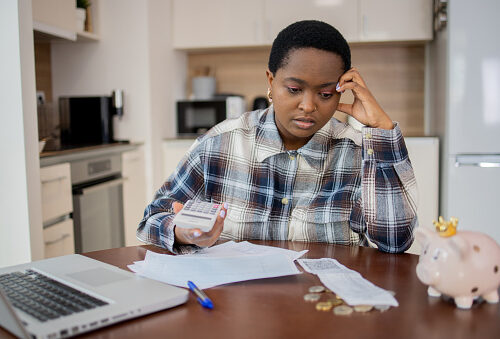

After the festive season, our money decisions came back to haunt us in January as some of us found ourselves going over budget for unnecessary things.

Spending time with loved ones can sometimes cause one to overspend and be too generous without looking at their bank balance and well some people tend to go into debt trying to splurge on things they cannot afford these choices hit many of us hard in the new financial year.

According to financial hub, Nedbank, to achieve financial success, you must be disciplined and committed to your goals. By adhering to your strategy and concentrating on your objectives, you can feel empowered and attain the outcomes you desire.

My Money Coach adds that this financial success can be achieved by you setting reasonable financial goals in the new year, adding that, you should concentrate on specific accomplishments rather than fast fixes.

Financial hub, Investopedia advises, “Consider whether you need more or less life insurance and whether your needs would be better satisfied by term or permanent life insurance.”

The above-mentioned source also mentions that to not crash out financially in January you need to set up an automatic transfer from your paycheck into a designated savings account. By doing this, a specific percentage of your earnings will be consistently saved before you even have the chance to consider the money as available for everyday expenses. This proactive approach to savings can help you build a financial cushion while keeping your spending in check.

WATCH THIS FOR WAYS TO SAVE IN JANUARY:

Also see; Stacking habits for a successful future at Momentum’s Science of Success Festival